A2P SMS for BFSI: Use Cases, Compliance Requirements, and What Your Infrastructure Must Support

Mohit Selly

In banking, NBFC, insurance, and fintech operations, a text message is rarely just a text message. An OTP that arrives ten seconds late can cost a customer a transaction. A fraud alert that never lands can cost them their savings. A delivery report that doesn't reconcile can cost an audit. This is the world A2P SMS for BFSI has to operate in, and it's a different world from the one most SMS platforms are built for.

This guide walks through where A2P SMS fits across BFSI sub-verticals, what compliance and delivery standards apply in India, and what separates infrastructure that's merely (SMS-capable) from infrastructure that's actually BFSI-grade.

What Is A2P SMS and Why Does BFSI Depend on It

A2P (Application-to-Person) SMS is messaging sent from a business system, a core banking platform, a loan origination system, or a claim engine; directly to a customer's mobile number, without a human typing the message on the other end. It's the channel behind OTPs, transaction alerts, EMI reminders, and policy communications across nearly every regulated financial institution in India.

BFSI depends on A2P SMS more heavily than almost any other sector because SMS remains the one channel that works without an app, without data connectivity in some cases, and without a customer opting into anything beyond having a phone number. For time-critical, compliance-linked communication, that universality is non-negotiable. A push notification assumes an app is installed and open to notifications. Email assumes an inbox is checked promptly. SMS assumes nothing except a working SIM, which is precisely why regulators and risk teams keep coming back to it as the channel of record for OTPs and fraud alerts.

The 6 Core A2P SMS Use Cases Across BFSI Sub-Verticals

Across banking, NBFCs, insurance, and fintech, the same channel gets used differently depending on the regulatory pressure and customer journey involved:

- OTP and transaction authentication: login, payment, and high-value transfer verification

- Fraud and security alerts: suspicious login attempts, SIM swap warnings, unusual spending pattern notifications

- EMI and repayment reminders: due-date nudges and overdue notices for loans and credit products

- KYC and onboarding updates: document status, re-KYC reminders, account activation confirmations

- Policy and claims communication: premium due dates, renewal reminders, and claim status updates for insurers

- Account and statement notifications: balance alerts, statement availability, scheme maturity notices

Banking and NBFCs lean hardest on use cases 1, 2, and 3, where transaction velocity is high, and failure has immediate financial consequences. Insurance leans on 4 and 5, where the cadence is slower, but the compliance stakes around proof of communication are just as real; a missed renewal reminder can become a dispute over lapsed coverage. Fintech platforms, often running thinner compliance teams than legacy banks, tend to need all six simultaneously, which is where infrastructure gaps show up fastest.

Compliance and Regulatory Requirements for A2P SMS in BFSI India

Indian A2P SMS for regulated financial communication sits at the intersection of telecom regulation and financial sector oversight. Three requirements come up consistently for BFSI senders:

DLT (Distributed Ledger Technology) registration is mandatory for any commercial sender of A2P SMS in India. Telemarketers and businesses must register their entity, headers, and message templates on the DLT platform before sending, and unregistered traffic is liable to be blocked at the telecom operator level. For BFSI senders, this isn't a one-time setup; template drift (a slightly reworded OTP message, a new claims notification format) without re-registration is one of the most common causes of sudden delivery drops.

Grey route risk is a related but distinct problem. Grey routes are unauthorised, non-compliant paths that some aggregators use to push messages more cheaply or faster, bypassing proper telecom interconnect agreements. For BFSI senders, grey-routed OTPs and alerts carry real exposure: inconsistent delivery, no reliable audit trail, and regulatory risk if a financial institution can't demonstrate its communication channel was compliant end-to-end.

The third requirement is less about a specific mandate and more about a posture BFSI institutions are expected to maintain in line with current RBI guidelines and sector-specific data handling expectations: demonstrable delivery proof and audit trails for every compliance-linked message, plus encrypted transmission for anything carrying authentication data. As a working definition for any IT or compliance team evaluating vendors, A2P SMS in banking refers to system-originated, DLT-registered, auditable messaging used for time-sensitive financial communication, as distinct from promotional or conversational SMS traffic.

SMS gateway setup is the natural starting point for institutions building or auditing this compliance posture from the ground up, since registration, header management, and routing configuration all happen at the gateway layer.

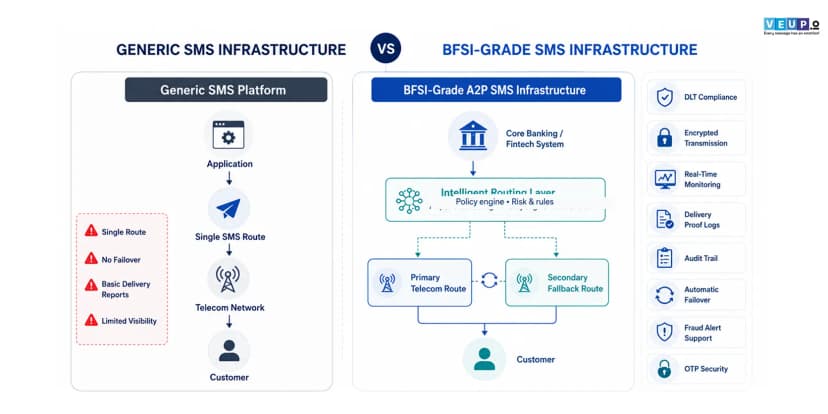

What Separates a BFSI-Grade SMS Infrastructure from a Generic One

Most A2P SMS platforms can technically send a message. Far fewer can guarantee it arrives, prove that it arrived, and recover gracefully when the primary route doesn't work. That gap is exactly where BFSI-grade infrastructure earns its name.

A generic SMS platform typically offers single-route delivery, basic delivery receipts, and minimal visibility into why a message failed. A BFSI-grade platform is built around a different set of assumptions: that failure will happen at the telecom layer regardless of how good the sender's system is, and that the infrastructure's job is to detect and route around it before the customer notices.

In practice, this means intelligent routing across multiple telecom paths, real-time delivery monitoring rather than batch reporting, and a fallback mechanism that activates automatically, not one that requires a human to notice a spike in failed OTPs and manually intervene. OTP engine security becomes a related but separate concern here: routing reliability gets the message moving, while encryption, rate-limiting, and replay protection keep it safe once it's moving. BFSI infrastructure needs both, and platforms that only solve one of the two leave a gap that eventually surfaces, either as a fraud incident or a failed audit.

How VeUp Powers A2P SMS for BFSI at Scale

VeUp's Omnichannel Platform is built around the assumption that BFSI communication needs to survive telecom-layer failure, not just function when conditions are ideal. Three components do the work:

- VeVault OTP Engine handles authentication-grade messaging with encrypted transmission and the kind of delivery-proof logging that compliance and audit teams ask for during reviews, without requiring banking and fintech clients to build that logging layer themselves.

- Velocity middleware sits underneath, intelligently routing every message across available telecom paths and making real-time decisions about which route gives the highest delivery probability for a given message at a given moment, rather than relying on a single static route.

- DLT-compliant template and header management is built into onboarding rather than left to the client to track manually, which matters most exactly when a BFSI institution updates a message template and needs that update reflected on DLT registration without a gap in deliverability.

Together, these mean a bank, NBFC, insurer, or fintech platform isn't stitching together a compliance posture from multiple vendors: registration, routing, fallback, and audit trail sit inside one system. For a regional NBFC processing thousands of daily EMI reminders and OTPs, that consolidation is often the difference between a 2 a.m. delivery incident getting silently rerouted versus getting escalated to an on-call engineer. → Talk to VeUp about BFSI-grade A2P SMS infrastructure

Common A2P SMS Failures in BFSI (and How to Prevent Them)

- The most expensive A2P SMS failures in BFSI are rarely dramatic outages; they're quiet, partial degradations that go unnoticed until a customer complains or an audit flags a gap.

- Silent OTP drop is the most common failure mode: a message is accepted by the sending platform but never reaches the handset, with no automatic retry or rerouting. The customer assumes the system is broken; the support team has no visibility into why. The fix is fallback routing for critical alerts, infrastructure that detects non-delivery on a primary route within seconds and reroutes automatically, rather than waiting for a manual escalation.

- Template mismatch with DLT registration happens when a message body is edited, a wording tweak, or an added variable, without the corresponding DLT template being updated, causing operators to block delivery. Preventing this requires treating template changes as a compliance event, not just a copy edit, with registration checked before any new template goes live.

- SIM swap blind spots occur when a fraud alert or OTP is sent to a number that's been fraudulently ported, and the sending system has no signal to flag the anomaly. While SMS infrastructure alone can't fully solve this, pairing delivery telemetry with anomaly detection on delivery patterns gives fraud teams an earlier signal than relying on the message channel in isolation.

- Treating SMS as a single point of failure is the underlying mistake behind most of the above. Institutions that route 100% of compliance-critical messaging through one provider, one route, with no fallback, are accepting a level of risk that's avoidable with the right architecture.

Conclusion

Frequently Asked Questions

Related Posts